Unlocking Opportunities in Private Equity Secondaries: Your Path to Success

Continuation vehicles (CVs) can be a useful liquidity tool—but their economics often favor GPs more than LPs might realize. In this article, we break down how CVs work, why they’re controversial, and what secondaries investors should watch out for when it comes to alignment and incentives.

4/11/20252 min read

In our view, continuation fund (CV) economics are pretty skewed in favor of GPs. So much so that it often takes additional measures to properly align incentives. Let’s walk through how continuation fund economics work - and why they’re controversial - using a simple example.

Example

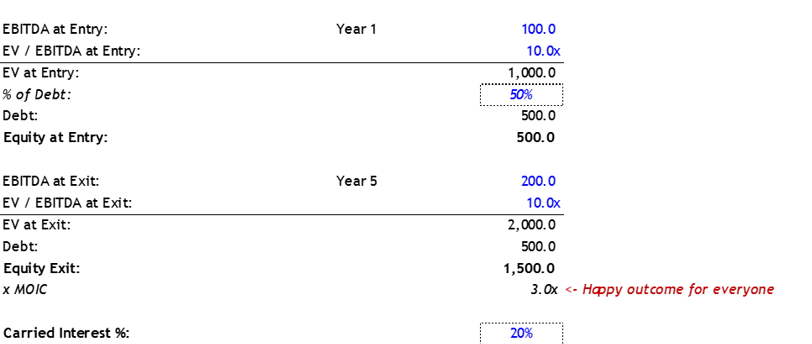

Let’s say a GP invested in a company in Year 1. The company does $100 million of EBITDA, and the GP buys it for 10x, putting in $500 million of equity.

Fast forward to Year 5. The company doubles its EBITDA, and it is valued at 10x. With the same debt amount, the equity is now worth $1.5 billion. That’s a 3x MOIC for the fund.

Implied GP carry? $200 million (20% of the $1 billion gain). At this point, the GP decides to run a continuation vehicle (CV) on this asset.

What Happens When a GP Launches a CV?

When a continuation fund is set up, the economics essentially reset. This generally means two things:

The GP rolls carry – In this case, the GP reinvests its $200 million of carry into the CV. That’s around 15% of the new vehicle - good skin in the game.

Management fees reset – The GP now charges a management fee on the CV’s purchase price, typically at a lower rate (say 1%). But the management fee base is now $1.3 billion instead of $500mn. And if there’s an unfunded commitment (say 20% of NAV), fees could be based on $1.56 billion total.

Assuming the asset stays in the CV for 5 years, that’s $78 million in management fees – enough to recover 39% of the GP’s rolled carry.

So What’s the Issue?

Let’s look at a few scenarios.

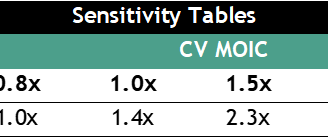

If the CV generates a 2.5x return - a typical target for single-asset CVs - the GP walks away with a 4.1x return. That’s a lot, but LPs might be fine with it since everyone’s making money.

But here’s the kicker: even if the CV only returns 1.0x, the GP still makes 1.4x from fees. Even if the CV generates 0.8x, the GP doesn’t lose money.

That’s why we think CV economics are tilted too far in the GP’s favor.

Sure, the GP is rolling meaningful carry and has skin in the game. But because they collect significant fees along the way, they may be incentivized to push even mediocre deals into a CV.

Final Thoughts

We’re not saying continuation funds are bad. They’re actually a solid liquidity tool when used correctly. But secondaries investors should go in with eyes wide open.

This is also why many secondaries buyers ask for more than just rolled carry. They often require GPs to commit fresh capital—say, from their next flagship fund—to ensure true alignment.